Tariffs on, Tariffs off, Tariffs on

Trump’s Tariff Moves: What Investors Need to Know About Trade War Risks in 2025

The Market’s Karate Kid Delusion

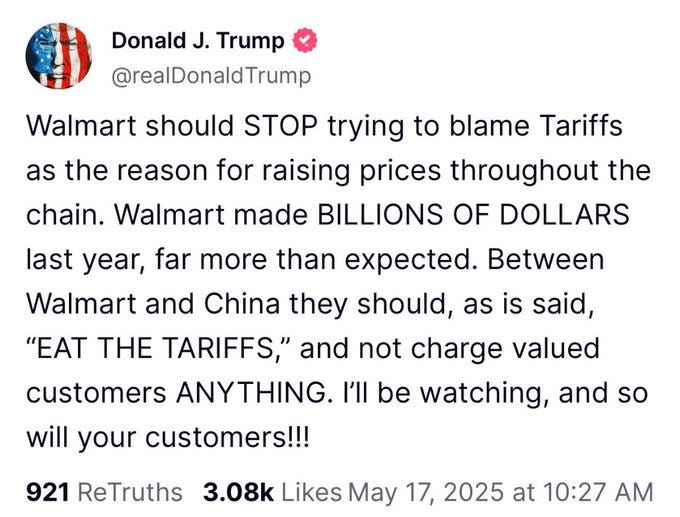

April 2 was “Liberation Day,” declared President Trump, as he slapped a blanket 10% tariff on every import—and rolled out extra punishments using the now-famous formula. China, having dared to retaliate, got the deluxe package: more than 100% tariffs for its insolence.

The market responded with a perfect nose dive—S&P 500 down from 5,670.97 to 4,982.77 in six days. Recession alarms went off. Yields spiked. And somewhere between a Treasury tantrum and an angry call from Wall Street, the administration blinked. The harsher duties were quietly paused—except for China, which remained in the penalty box.

Trump, of course, claimed victory. This was 4D chess, he explained. Hundreds and hundreds of countries (there are only 195, but never mind) were lining up to strike deals. Tariffs, it turned out, were not a blunt instrument—they were leverage. Peter Navarro confidently promised on April 11 “90 deals in 90 days,” as if this were a discount sale at Bed Bath & Beyond.

90 deals in 90 days

This sounds great. But I was skeptical, to say the least.

For perspective: the U.S.–Mexico–Canada Agreement—between three befriended neighbors sharing power grids, and supply chains—took 471 days to hammer out.

If that’s the timeline for friends, it seems fair to assume that deals with rivals might stretch a little longer.

So how many deals do we have so far? (And to be clear: a deal is not a trade agreement.)

One is with the UK—a press release dressed as policy. It ends with a quiet disclaimer:

Both the United States and the United Kingdom recognize that this document does not constitute a legally binding agreement.

The other is a handshake in Geneva: a 90-day pause on the U.S.–China tariff escalation. Not a framework, not a treaty—just an agreement to continue to talk to each other.

And the market? It shrugged, forgot everything, and floated back to 5,958.38, as if none of this ever happened. Like a goldfish with a margin account.

But the world is a different one now.

From absolutely insane to merely crazy

But after all that’s good news—are we back to square one?

Not at all. After the partial pullback, the average U.S. tariff still sits at 17.8%—the highest since 1934.

Paul Krugman summed it up neatly:

America has moved from a completely insane tariff rate to a rate that’s merely crazy

The straitjacket now has looser sleeves. Progress?

Tariffs off again? Not quite.

Just when we thought tariffs were off, they’re back on. The Karate Kid returns.

The idea that the administration has shelved its tariff crusade is wishful thinking. Having discovered that negotiating with 150 governments at once is unworkable, the President now (May 16) proposes a simpler fix: send everyone a letter.

Each country will receive a customized note outlining its new rate. “Very fair,” he promises. Less diplomacy, more bulk mailing.

But don’t be fooled—tariffs are still front and center. In my personal experience, the longer someone clings to an idea, the harder it gets to let go1. After forty years of calling tariffs the answer to everything, this president isn’t likely to walk away now.

The real risk still lies ahead.

One small personal announcement: I’ve added a 75% discount for students and educators—valid for the next two weeks only.

Thank you for your work in teaching, learning, and keeping the pursuit of knowledge alive—especially at a time when universities are under political attack. In light of recent rhetoric targeting places like Harvard, this one’s for you.

Thanks to Robert Wu for making me aware of this new Substack discount feature and encouraging me to set this up.

Skate to Where the Puck Is Going

The market, as usual, is skating to where the puck was. Judging by the full recovery in equity prices, investors now seem to believe the world is somehow safer than it was before Liberation Day. I beg to differ.

I’ve adjusted my own probability distribution. While I still assign a non-zero probability that Trump might backpedal and things resolve peacefully, that path looks narrower by the day. In contrast, the probability of prolonged trade frictions—and negative economic outcomes that will only reveal themselves over time—has meaningfully increased. Supply chain disruptions don’t show up overnight. At the earliest, they’ll start surfacing in second-quarter earnings. Empty shelves, pricing distortions, and margin pressure will likely begin creeping into view in the coming weeks.

From drill baby drill to eat baby eat?

I’ve adjusted my probability distribution accordingly. The expected value today looks worse than it did on April 1—even if the market insists otherwise.

Block Out the Noise

Still, obsessing over every twist in the tariff saga is a poor use of time. The signal is noisy, the reversals are constant, and nothing is truly settled until it’s not only announced—but implemented, enforced, and survived a news cycle. Even then, as the Canada–Mexico agreement—negotiated by Trump himself during his first term—showed, a signature today can still be undone by a tweet tomorrow. So better to focus on what we can actually control.

Right now, the market is punishing some companies simply for existing in a jittery environment—despite having no direct exposure to trade. Sure, if the global economy takes a nosedive, even domestic businesses will feel it. But that’s a second-order effect. And not all second-order effects justify first-order panic.

So I’ve given myself a break from reading news these days. No more tariff alerts, no more tea-leaf reading. I’d rather spend that energy looking for mispriced assets than decoding another mail-merge from the White House. Blocking out the noise isn’t denial—it’s focus.

And when the market swings back to the pessimistic side—as it always does—be ready. That’s when the real bargains show up.

Some other article you might like:

That’s why the Fields Medal has an age limit—after 40, your brain just doesn’t want to do new things anymore. You start looking at everything the same way. Which is also why they say a mathematician’s career is basically over by then.