Learning from Walter Schloss: Crafting Your Unique Investment Strategy

Why do famous investors have contradictory approaches, and why do they still work out for them?

Summary:

I discuss why finding your own path in investing is crucial and how blindly quoting others to justify your investment decisions can be a poor strategy. I will detail how even famous investors, who have made significant amounts of money, often disagree on many aspects of investing and explain how they can still succeed financially despite their differing opinions.

An interview with Walter Schloss

Recently, I re-watched an interview with Walter Schloss. His down-to-earth personality is refreshing and quite different from today’s talking heads. Many people who watch the video point out that he constantly says,

I don’t like to lose money.

— Walter Schloss —

While this is an important message, another point caught my eye.

When asked if he talks to management, Schloss simply says no. His reason is straightforward: he is not good at judging people. He knows his limits. He points out that Warren Buffett excels at this, so Buffett benefits from engaging with management, while Schloss does not.

Schloss realized that the key is to develop your own unique investment style rather than blindly following others, as you must do what works best for you and aligns with your personality.

This made me reflect on a recent experience I had.

Dinner with the Name-Dropper

I had dinner with a guy who once visited Charlie Munger’s house. He could not complete a sentence without saying Warren, Charlie, or Peter (Lynch), as if these famous investors reported to him daily (even posthumously in Charlie's case).

First, I thought, “Fuck me.” Then my mind went blank, and the only thing I could do was count in how many sentences he said “Warren” or “Charlie.”

I figured it would be easier to count the sentences where he didn’t say their names. This gave me the idea that it would make a terrific drinking game: every time he mentions one of them, take a shot - but I digress. What he said? Don’t ask me I was busy counting!

From my observation—whether in investing, academia, or life in general—people who constantly refer to famous individuals to support their arguments are often the biggest losers. Intelligent people can think independently. They don’t need to claim support from famous figures to avoid criticism or to make their points carry more weight.

The Pitfalls of Relying on Famous Quotes

Why do I bring this up? I think that in investing, more than in any other field, relying on quotes from famous people is a fool’s errand. In chess, it might be good to follow what Magnus Carlsen says, but in investing, doing what famous people say often backfires.

Chess is vastly different from investing in that good chess players would generally agree on the best moves, at least to some extent, and whatever they agree on would indeed be a good move. In investing, if famous investors agree on an idea, it’s far from certain that it will work out, and more often than not, they would actually disagree on those idea.

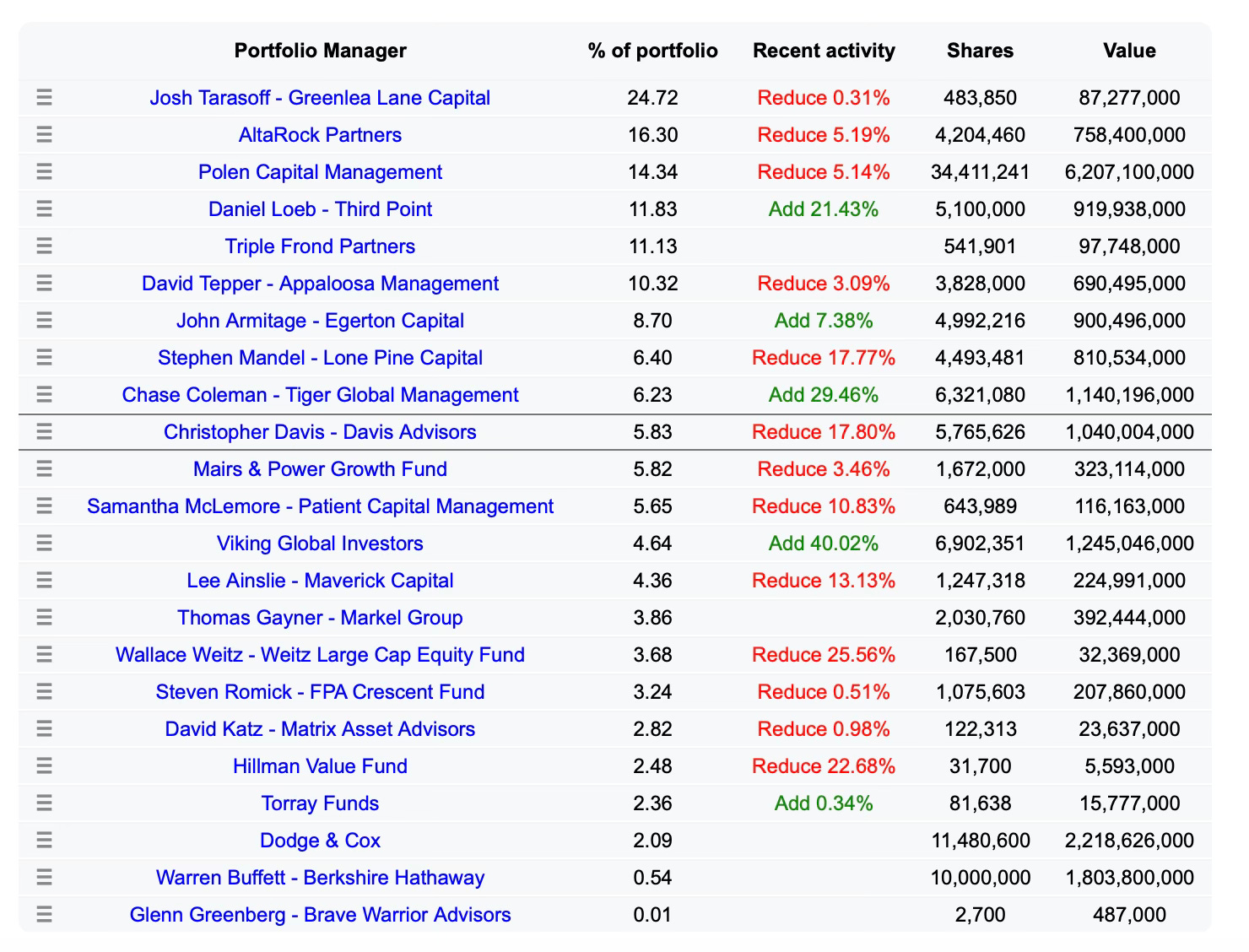

Look at some recent activity with Amazon stock, but you can choose any other stock you want—it will look similar. Some people are buying, and some are selling. So, who is right about Amazon? (Interestingly, all of them could be right. It depends on your opportunity set, but that is not the topic of this article.)

In investing, even the best are rarely more than 70% correct. What truly matters is not just being right, but by how much you are right or wrong. Even being correct less than 50% of the time can be highly profitable if your gains outweigh your losses.

But don’t just take my word for it; see what the best investors have to say about different topics in investing. Here are some quotes from famous investors who all made significant money in the stock market but seemingly can’t agree on a single thing. If one person says something is good, another says exactly the opposite.

On Diversification:

Warren Buffett: Diversification is protection against ignorance. It makes little sense if you know what you are doing.

Peter Lynch: The key to making money in stocks is not to get scared out of them. Diversification is important.

On the Research Process:

Warren Buffett: We are looking for businesses we can understand, with favorable long-term prospects, operated by honest and competent people, available at a very attractive price. We are looking for companies that have a long-term predictable cash flow.

Stanley Druckenmiller: Buy first, analyze later

On Market Timing:

Peter Lynch: Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.

Peter Lynch: Don’t bottom fish.

Paul Tudor Jones: I believe the very best money is made at the market turns.

On Investment Approach:

Warren Buffett: Our favorite holding period is forever.

George Soros: Markets are constantly in a state of uncertainty and flux and money is made by discounting the obvious and betting on the unexpected.

On Technical Analysis:

Jim Rogers: I haven’t met a rich technician.

Marty Schwartz: I always laugh at people who say, ‘I’ve never met a rich technician.’ I love that! It is such an arrogant, nonsensical response. I used fundamentals for nine years and then got rich as a technician.

Apparently, they can’t agree on anything: technical analysis, diversification, research process, or market timing. From this, you can see that no matter what you want to do, there is a quote out there that confirms what you’re doing right now.

Let me give you an example. So you bought a stock and after that it goes down in price. What do you do?

Do you go with Warren Buffett?

If the stock goes down, we can buy more shares. I like it when stocks go down after I buy them initially.

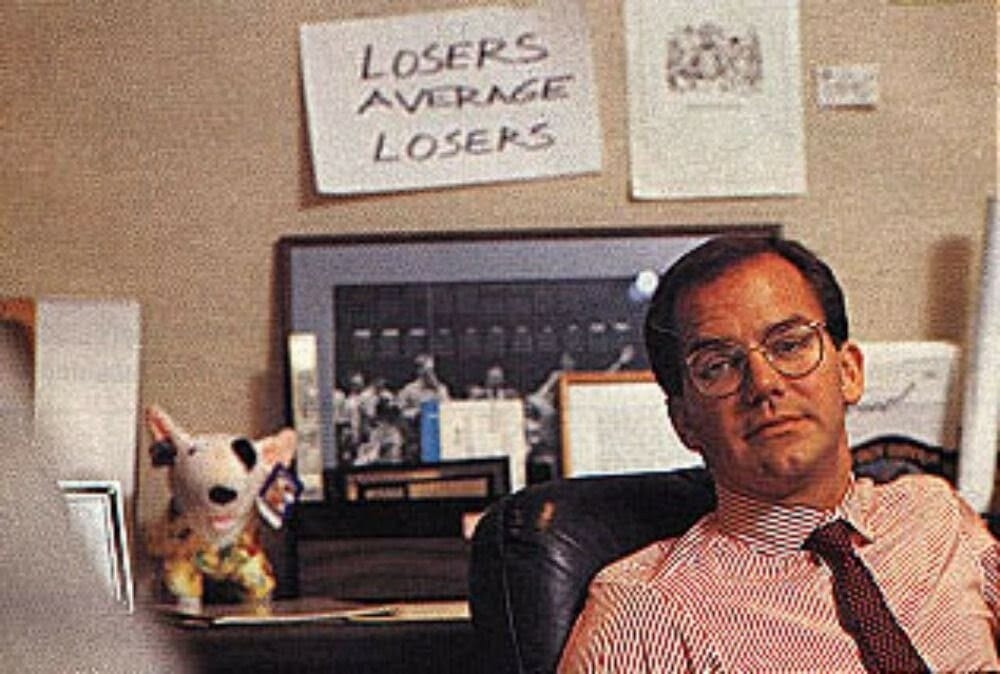

Or do you go with Paul Tudor Jones?

Losers average losers.

Finding Your Unique Investment Path

In investing, there is no single correct way to succeed. People with completely different, even contradictory or complementary approaches, have made huge amounts of money in the stock market. As Walter Schloss said, what matters is finding a style that matches your personality. What works for one person might be entirely wrong for another.

Quoting famous people is only useful if you understand the context and strategy behind their success. Instead of quoting investors at random, first figure out whose approach aligns with your own strategy and personality.

Comment on Buffett selling Apple:

Let me briefly comment on Warren Buffett selling a significant portion of his stake in Apple. At the time of writing, he has probably sold another large chunk, and if prices continue keep up, I wouldn’t be surprised if he is completely out of Apple by the time he files his next 13F report. Notably, he sold Apple without any other major investment in sight, at least as far as we can predict from his cash holdings.

While Apple is indeed richly valued and the rise of AI could be a factor, I don’t believe these are the main reasons for his decision. Apple has been richly valued for some time now. I think this move is actually a strategy to de-risk from China. In the third quarter of 2022, Buffett bought shares in Taiwan Semiconductor Manufacturing Company (TSMC) but sold most of them the very next quarter, citing changes in his view of the geopolitical situation between Taiwan and China. He has also been reducing his position in BYD.

Among American companies, Apple has the greatest exposure to China. China is not only one of Apple’s biggest markets, but it is also where most of its production is based, making Apple more dependent on China than companies like Amazon, Google, or Facebook.

These are my thoughts, but I’m happy to hearing your comments and any disagreements you might have.

Agreed, really like how you mentioned ‘Intelligent people think independently’. You have to understand and play to your own unique strengths and weaknesses.

I think I mostly agree. It's helpful to learn from the techniques of all of the greats.

I think like most professions, you choose the techniques relevant to your personal context and the surrounding environment at the time to achieve the goals. There are no bonus points to being dogmatic.